How to Write a Check (Yes, It's Still a Thing)

Not sure how to fill out a check? Here's a quick breakdown of every part.

Key takeaways

- Checks remain relevant for large payments, landlords, contractors, and situations requiring documentation.

- A properly written check includes six key elements: date, payee name, numerical amount, written amount, optional memo, and your signature.

- You can protect yourself from fraud by using gel ink pens, avoiding blank spaces, and storing your checkbook securely.

If you've ever found yourself staring at a blank check, unsure which line is for what, you're not alone. In an era of tap-to-pay and instant transfers, check-writing has become one of those skills many people never quite learned—or simply forgot from lack of use.

The good news: it's straightforward once you know the basics. And despite the rise of digital payments, there are still plenty of situations where knowing how to write a check comes in handy.

How to write a check, step by step

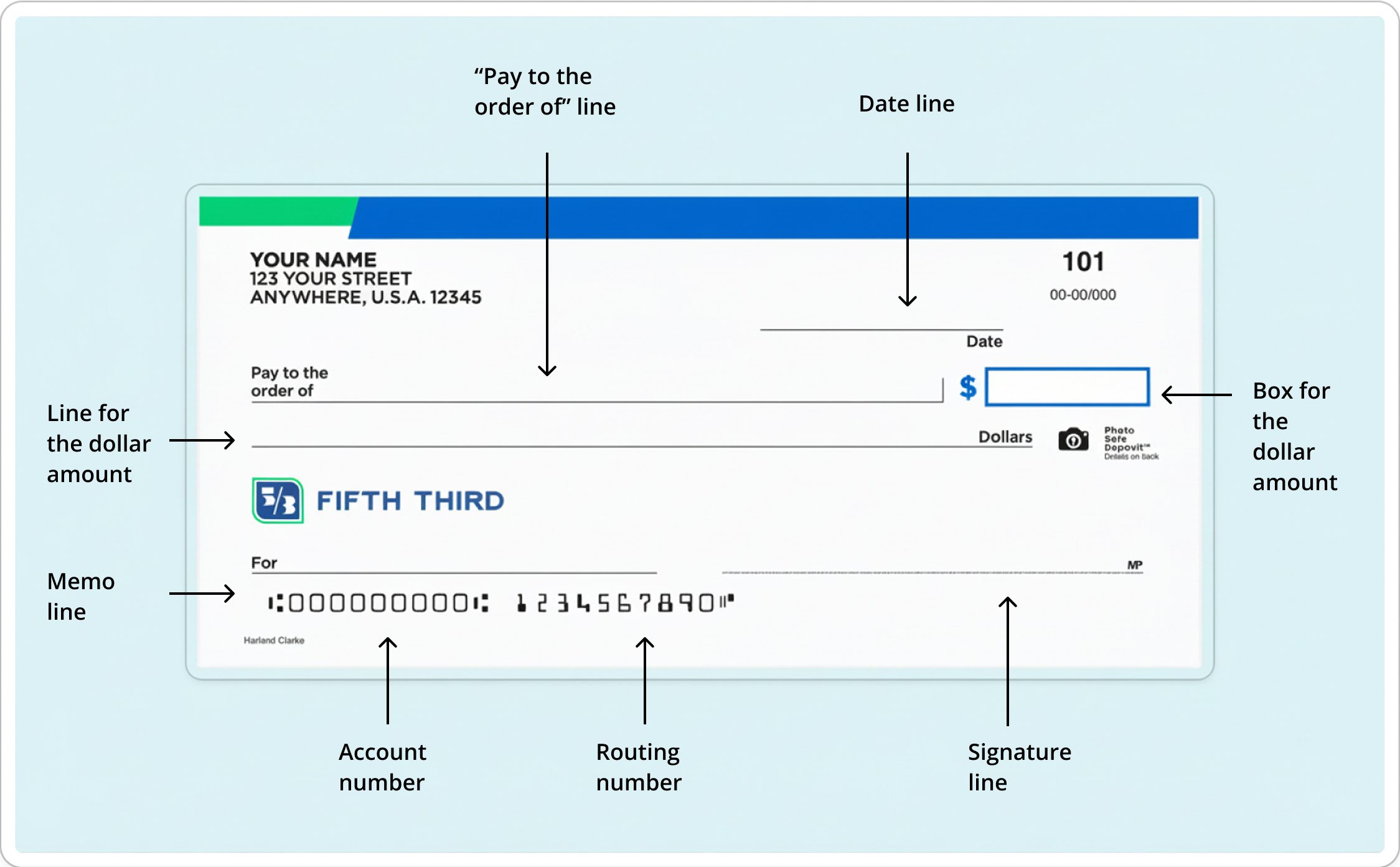

Here's a breakdown of each field on a standard personal check:

- Pay to the order of (the long line): This is who gets the money. Write the full name of the person or business receiving the payment. If paying a business, confirm the exact legal name—"Jim's Plumbing" and "James Smith Plumbing LLC" are different entities as far as banks are concerned.

- Date (top right corner): Write today’s date. You can post-date a check if you want, but know that banks don't always honor that and might process it early anyway.

- The dollar amount in numbers (the small box): Enter the amount using numbers: $150.00. Include cents even for whole-dollar amounts to help prevent alteration.

- The dollar amount in words (the line below the payee): Spell out the dollar amount: "One hundred fifty and 00/100." The fraction represents cents. Draw a line through any remaining space to prevent additional words from being added.

- Memo line (bottom left, optional): This line is for your reference. You can note the purpose of the payment—"January rent," "Invoice #4521," or an account number. While not legally required, it helps with record-keeping.

- Your signature (bottom right): Sign exactly as your name appears on your checking account. Without a signature, the check cannot be processed. This is also why signing a blank check is never advisable.

Protecting yourself from check fraud

Write in pen, preferably gel ink, which is more difficult to alter. Avoid leaving blank spaces that could be filled in. Store your checkbook securely, and don't leave outgoing checks in an unlocked mailbox. For mailed payments, consider dropping them inside the post office.

For large or recurring payments, checks can actually offer more control than automatic withdrawals. You determine exactly when the money leaves your account, and you maintain a physical record of each transaction.

When checks make the most sense

Despite the digital revolution, checks remain practical in several situations:

- Large one-time payments. Tuition, down payments, contractor deposits—these often work better as checks than credit cards (which may incur processing fees) or debit transactions.

- Gifts. Mailing cash carries risk. A check is more secure, and recipients can typically deposit it instantly using mobile banking.

- Payments to small businesses. Many local contractors, cleaners, and service providers either don't accept cards or charge fees for card payments. Checks avoid those additional costs.

- Transactions requiring documentation. Legal settlements, charitable donations for tax purposes, or any situation requiring clear payment records.

Who's still writing checks?

Federal Reserve data shows clear generational patterns. According to a 2025 report from the Federal Reserve Bank of Atlanta, 65% of consumers aged 65 or older reported writing a check in the last month, compared with just 4.7% of consumers aged 18-24.

The generational divide makes sense. Older adults grew up when checks were standard for everything from groceries to rent. Younger generations came of age with options like Zelle® and mobile wallets.2 But knowing how to write a check remains a practical skill. You may not need it often, but you’ll appreciate having the knowledge when the situation arises.

It's worth noting that checks still account for a meaningful share of bill payments specifically. When it comes to paying rent, tuition, or contractors, checks remain among the most commonly used payment methods, particularly for transactions where the payer wants control over timing and documentation.

Quick tips for check-writing success

A few practical reminders:

- Keep a register. Most checkbooks include a paper register to track payments. This remains useful because digital banking apps don't always reflect pending checks immediately, and tracking them yourself helps prevent overdrafts.

- Use the memo line strategically. For bills, include your account number. For rent, include the month and property address. For gifts, a brief note adds a personal touch.

- Order checks through your bank. Third-party check printers may cost less, but checks from your bank include security features that help prevent fraud.

Bottom line

The financial world is clearly moving toward digital payments. Mobile transactions are up, and check usage continues its gradual decline. But "declining" doesn't mean "obsolete." The Federal Reserve still processes billions of checks annually, representing trillions of dollars in transactions.

So keep that checkbook handy, and now you'll know exactly how to write one when the moment arrives.

Learn more: Looking for a checking account with check-writing abilities? Explore Fifth Third's checking options to find the right account for you.