From Cash to Code: Stablecoins in the Age of Digital Finance

Key Takeaways:

- Stablecoins bridge traditional finance and blockchain, offering fast, low-cost transactions.

- New U.S. laws boost stablecoin growth, with clearer rules and stronger oversight.

- Stablecoins may reshape global finance, but their success depends on trust, regulation and integration with existing financial systems.

As financial markets become increasingly digital, stablecoins have become a key bridge between traditional finance, investment strategies and blockchain. Pegged to fiat or asset pools, they combine the stability of cash with the efficiency of digital assets, attracting interest from banks, payment networks, merchants and consumers. With legislative momentum building, understanding stablecoins is becoming essential to navigating the future of money and monetary policy.

What are stablecoins?

In 2008, Satoshi Nakamoto published a seminal white paper introducing Bitcoin and launching the era of decentralized digital currencies.1 While groundbreaking, Bitcoin’s volatility limited its use for transactions and wealth preservation prompting the creation of stablecoins. Like Bitcoin, stablecoins are traded on blockchains—digital ledgers that record transactions—but are designed to maintain a stable value through asset collateralization.

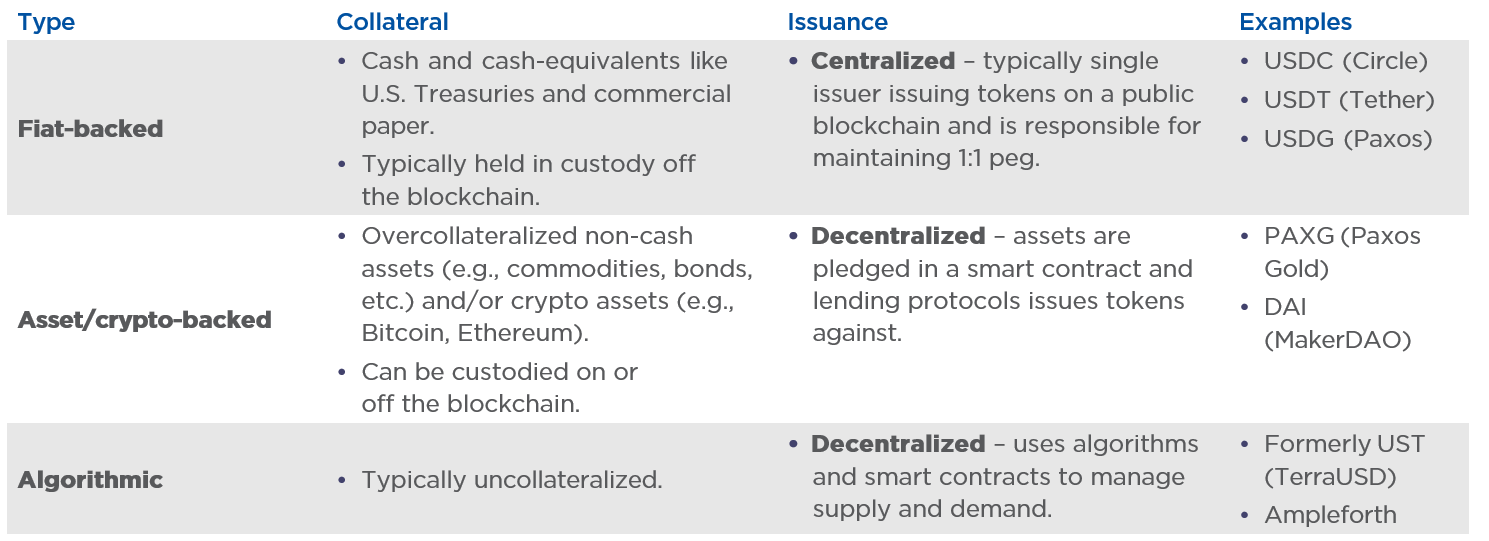

Exhibit 1 categorizes the main types of stablecoins by their collateral and issuance models.

Source: Cy Watsky, et al, “Primary and Secondary Markets for Stablecoins,” Federal Reserve, 2024, https://www.federalreserve.gov/econres/notes/feds-notes/primary-and-secondary-markets-for-stablecoins-20240223.html

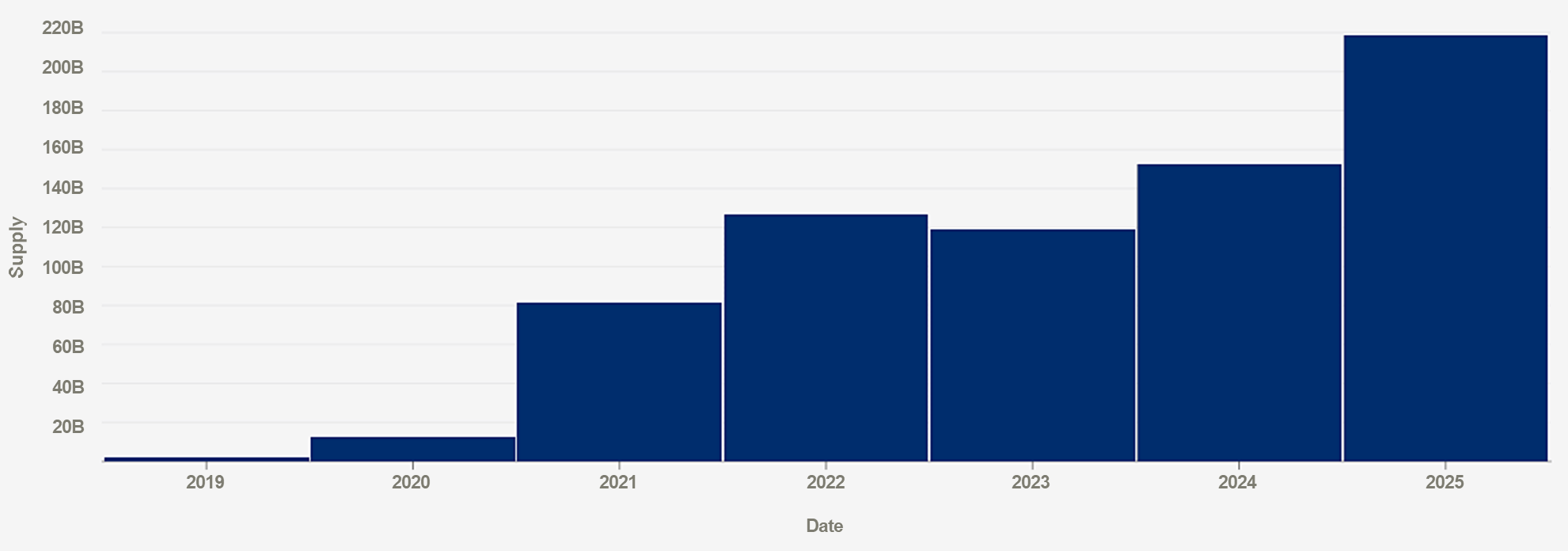

The first fiat-backed stablecoin, Tether (USDT), was launched in 2014 allowing users to deposit fiat currency with Tether Ltd. in exchange for a digital token—1 USDT—redeemable for the underlying currency.2 Acting as an on-ramp to the crypto ecosystem, stablecoins have seen rapid issuance growth, as shown in Exhibit 2, driven by investor demand for access to Bitcoin and other digital assets.

Exhibit 2: Average stablecoin supply, all stablecoins—by year.

Source: Allium, “Average Stablecoin Supply, by Stablecoin,” Visa Onchain Analytics Dashboard, 2025,https://visaonchainanalytics.com/supply

Why are investors excited about stablecoins?

July 2025 marked a turning point for stablecoin regulation. The GENIUS Act now law, established the first federal framework for payment stablecoins, mandating full reserve backing, issuer registration and compliance with anti-money laundering, know-your-customer and consumer protection standards. The CLARITY Act passed by the House, clarified digital asset market structure by assigning oversight of most tokens to the Commodity Futures Trading Commission, while preserving the Securities and Exchange Commission’s role in fraud prevention. Meanwhile, the SEC launched Project Crypto to modernize securities rules, enabling tokenized trading and blockchain-based custody. With these frameworks in place, stablecoin issuance is expected to accelerate—U.S. Treasury Secretary Scott Bessent projected the U.S. dollar stablecoin market could exceed $2 trillion by 2028.

Stablecoin use cases

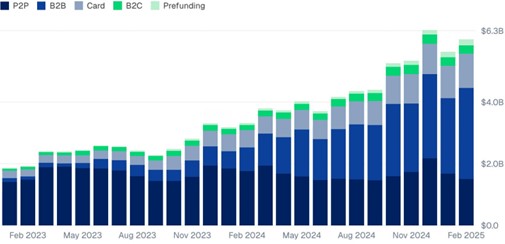

Financial institutions have been early adopters of stablecoins, using them to bypass slow and costly correspondent banking networks in cross-border transfers and tokenize deposits for 24/7 access to funds and near-instant settlement. For large merchants such as Amazon and Walmart, stablecoins offer the potential to transact directly with customers, bypassing interchange fees charged by payment processors and enabling instant settlement, which improves cash flow.3 Though concerns remain around cost, fraud risk and consumer adoption, businesses are increasingly using stablecoins to transact, as evidenced in Exhibit 3.

Exhibit 3: Businesses have quickly adopted stablecoins for payments - Stablecoin payments by type

Source: Artemis Analytics, “Stablecoin Payments from the Ground Up, ArtemisAnalytics.com, 2025, https://reports.artemisanalytics.com/stablecoins/artemis-stablecoin-payments-from-the-ground-up-2025.pdf

Monetary and fiscal implications

With over 99% of stablecoins referencing or backed by U.S. dollar-denominated assets, they increasingly function as quasi- sovereign monetary instruments, with the SEC now recognizing some as a form of cash.4 Continued growth in issuance will drive incremental demand for U.S. Treasuries as a form of backing, supporting further deficit financing and implicitly expanding dollarization alongside stablecoin usage.

“We are going to keep the U.S. the dominant reserve currency in the world, and we will use stablecoins to do that,” shares U.S. Treasury Secretary Scott Bessent.

While promising, there remain key hurdles to widespread stablecoin adoption and the potential risks associated with their use.

The consumer value proposition is weak

A major barrier to stablecoin adoption is consumers’ longstanding preference for traditional payment cards, driven by convenience, rewards and broad acceptance. In contrast, direct stablecoin usage requires familiarity with crypto wallets and interfaces, which can be intimidating or inconvenient. One solution is stablecoin-linked credit cards that allow consumers to spend stablecoin balances using cards issued by companies such as Visa and Mastercard. However, with few incentives and limited merchant acceptance currently, stablecoins lack the network effects needed to gain traction as a mainstream payment method.

Stablecoins are not always very stable

Tether, the largest stablecoin by market capitalization, has lost its $1 peg on several occasions, albeit only for brief periods, as has the stablecoin issued by Circle—most notably in 2023 following the collapse of Silicon Valley Bank5 Such dips have been limited to secondary market pricing and typically stem from banking system constraints that disrupt primary issuance, combined with large spikes in redemptions. For context, a large proportion of U.S. fiat deposits are uninsured by the Federal Deposit Insurance Corporation, making them vulnerable to run risk as well. During market panics, a surge in redemptions can force issuers to rapidly liquidate assets, potentially triggering a run and causing short-term yields to spike as collateral is sold. Recent legislation and regulatory frameworks are expected to help reduce this risk going forward.

Conclusion

Stablecoins are at a pivotal point in their evolution, with the potential to reshape global finance. As regulatory frameworks solidify, institutional adoption is accelerating and new models are emerging — including potential integration with central bank digital currencies and use cases tailored to specific financial functions. Their long-term success will hinge on balancing innovation, trust and regulatory compliance.

To learn more, contact your Fifth Third Private Bank advisor.